By Jess Ponting

As 2026 kicks off, it’s worth reflecting on what our industry has been through and where it is headed in the immediate term. Since the first Surf Park Summit in 2013, the industry has been grappling with the question, “Can surf parks even work at all?” At Surf Park Summit 2025, from very reliable sources outside the industry, we heard the answer. Yes. Yes, they can.

What will make the next 24 months different is not a single breakthrough or blockbuster project, but the convergence of external forces that are pushing surf parks into a new role—one defined less by novelty and more by scale, permanence, and relevance within broader leisure and real estate ecosystems. Multiple surf park developers and operators are pursuing multiple projects simultaneously in many different geographies. Many of these developers are technology agnostic, choosing the best solutions for each site and its demographic profile. Business models continue to evolve around a greater understanding of location demographics, particularly in the area of private clubs and amenitized residential, and mixed-use real estate.

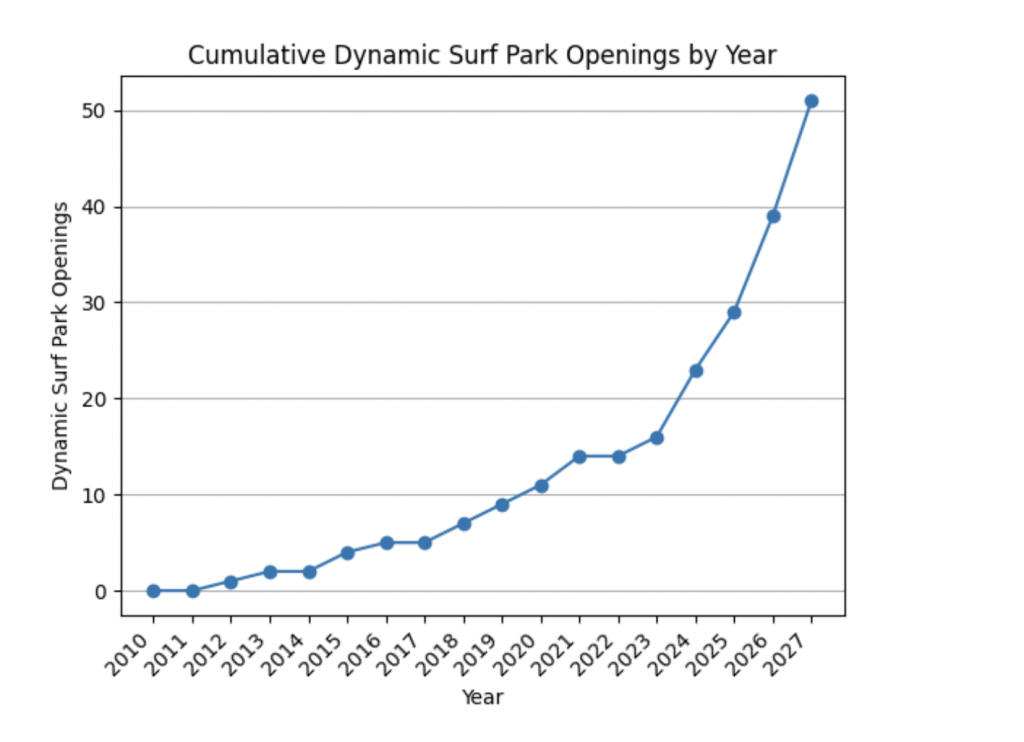

The surf park landscape is changing quickly. By the end of 2027, the current global inventory of 26 dynamic surf parks built between 2015 and 2025 is set to nearly double (or possibly even double) based solely on committed projects between Wavegarden and Endless Surf. In fact, Endless Surf appears poised to leapfrog American Wave Machines to take second place behind Wavegarden in terms of operating projects in 2027, if not 2026. Additionally, we expect projects from American Wave Machines, Surfloch, and Swell MFG to open in the same period.

Wave Generation Innovation Announcements at Surf Park Summit 2025

Leading wave-generating technology providers announced new innovations at Surf Park Summit 2025 that are facilitating industry growth as a wider variety of shapes and sizes of lagoons become available and new wave shapes are created that continue to improve the surfing experience.

For example, Surf Loch announced a new lagoon design called the WaveBender, which essentially arranges the backwall pneumatic caissons in a crescent shape, rather than a straight line. This configuration causes the energy being fed into a wave by each caisson as it travels across the lagoon to come from a more acute angle, causing the wave to bend in toward the surfer. This sensation will be familiar to surfers who have experienced a beach break ‘rip bowl’ or a reef break that refracts swell energy toward, rather than away from, the surfer. See the WaveBender rendering below. Even more exciting was the announcement that three WaveBender projects are underway, including one already under construction in São Paulo and others under contract but not yet under construction in California and Australia.

Surfloch’s WaveBender

In a classic ‘mic drop’ moment, the Endless Surf team unveiled both a new ES66 project in development near São Paulo, which will provide a best-in-class 40-second ride, and an impressive new wave shape designed by wave-making virtuoso and new addition to the Endless Surf team, Cheyne Magnusson. Cheyne’s new programming provides the tallest and throatiest, yet still approachable, barrel yet seen in an Endless Surf lagoon.

Directly after Endless Surf highlighted its ability to scale back wave production to suit periods of lower demand in ways that (though unspoken, the target was obvious), Wavegarden Cove cannot, Wavegarden produced a mic drop moment of their own. It was revealed that a new iteration of their electro-mechanical wave-generating system called ‘OneSwell’ is already in operation at the Wavegarden LAB in the Basque Country. This system does not require a central pier or huge volumes of concrete, and it very much can scale back to produce one wave at a time with controllable wave periods, using similarly small amounts of energy to the Cove per wave. Most remarkably, OneSwell does all this from a linear back wall from which Wavegarden’s familiar electro-mechanical paddles push waves into a lagoon shape reminiscent of most pneumatically driven surf parks. This new configuration completely changes the footprint required for a Wavegarden project and presumably erodes some of the previous points of difference between Wavegarden and its pneumatic competitors. The first commercial OneSwell is to be built in Costa Blanca, Spain, and four additional projects are reportedly in the early design stage of development.

Rendering of Wavegarden’s new OneSwell format.

São Paulo and The Rise of Amenitized Residential Developments & Private Clubs

A change that will reshape the industry over the next two years is the proportion of surf park projects in development that involve a private club business model, often combined with an amenitized residential real estate development. The model was pioneered in Brazil by Oscar Segall and KSM Realty at Praia da Gama, about an hour north of São Paulo city, powered by a Wavegarden Cove, opening in 2021. The model situates the surf lagoon as a lifestyle amenity anchor for a residential development that also includes an 18-hole golf course, horse riding, beach volleyball, tennis, gym, swimming, spa facilities, restaurants, a surf shop, event space, and agroforestry. The surf lagoon is private, only accessible to residents or members who pay a premium for access.

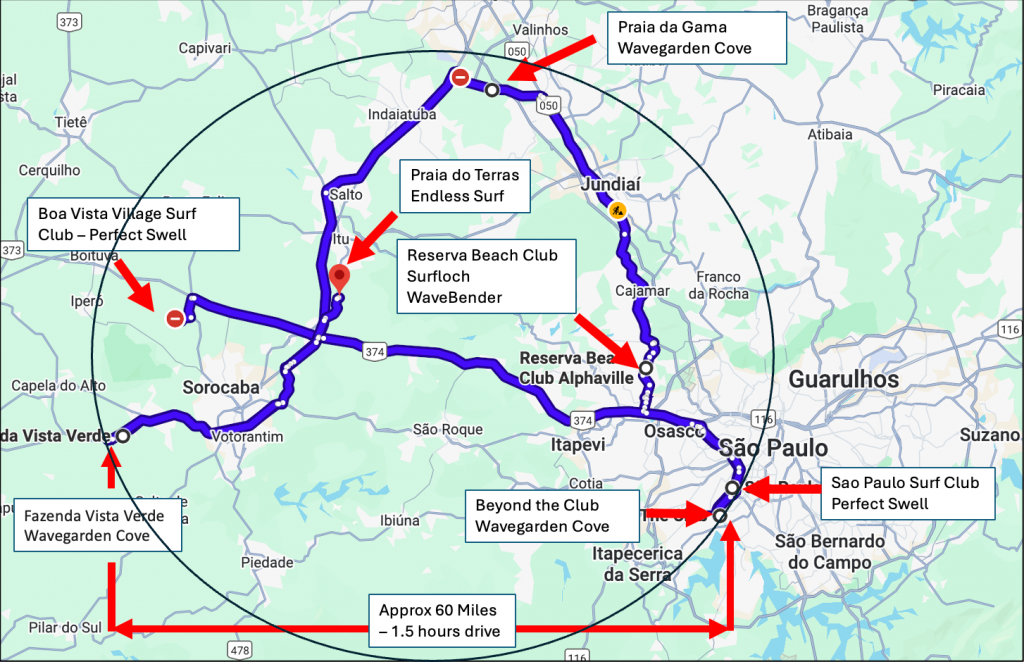

This private surf park model, catering to a relatively small, wealthy group of outdoor and adventure lifestyle enthusiasts paying high-end golf or country club equivalent membership fees and monthly dues, has proven very successful. Legend has it that undeveloped land values increased 10x, more or less overnight, with the announcement of the private surf lagoon as an anchor amenity at Praia da Grama. These rumoured returns and many other unique data points sparked a surf park gold rush in greater São Paulo. Subsequently, two surf parks have been built in São Paulo city within 4 miles of each other, and another an hour’s drive to the west. Three more are in development in the exact same region. All seven of these surf parks will be within a 60 mile radius and an hour and a half drive of each other. That is a pretty wild challenge to common assumptions about surf park market saturation. How can this possibly make sense?

The Seven Private Club Model Surf Parks in Greater São Paulo

São Paulo is one of the largest urban population centers in the world, with around 12 million residing in the city and a greater metropolitan population of around 22 million. Additionally, surfing is one of the most popular sports in Brazil, behind only soccer, volleyball and basketball, and the beach is a 1.5 hour drive away on the other side of a mountain range. While this all bodes well for traditional surf park business models, the annual individual median income in São Paulo is approximately USD$12,000 per year. Public surf park models currently completely dominate surf park inventory outside of Brazil. However, in most of these locations, individual median incomes are significantly higher: USD$50,000 in Sydney and California; USD$62,000 in Bristol; USD$71,500 in Munich; and USD$90,000 in Switzerland. Unfortunately, the distribution of wealth in São Paulo renders traditional public surf park models economically marginal at best. It should not therefore, come as a surprise that every single one of the seven surf parks in the greater metro area, built and planned, are ALL private club models. Every. Single. One.

Each includes an incredible array of additional amenities to the surf lagoon, virtually identical to Praia da Grama or even more extravagant. Most, with the exceptions of Beyond the Club and Reserva Beach Club, include significant residential real estate developments. Some insight is available into the cost and number of memberships with Boa Vista selling family memberships at USD$190,000, Beyond the Club at $125,000 for a family membership with 3000 memberships available (that’s a potential total of USD$375 million), while São Paulo Surf Club membership is USD$185,000.

Given the private club model numbers being generated in Brazil, the model is in the process of jumping the Brazilian shark. In addition to more private surf clubs coming as soon as this year to other parts of Brazil (e.g., Brazil Surf Club in Rio de Janeiro), we will see the Cabo Real Surf Club open in Mexico in 2026 and many more private models under construction including Zion Shores in Utah, Austin Surf Club in Texas, and Crest Surf Club in New York. Where private models are not being pursued, a massively increased focus on residential real estate, hotels, and expanded retail and FnB offerings is being integrated into every new surf park development. Or perhaps more correctly, surf parks are being incorporated into much larger integrated real estate developments – the Qiddiya development in Saudi Arabia being a singular case in point. The expected surge in surf park openings over the next two years will likely see surf parks that incorporate residential, hotel, or significant retail and FnB beyond the standard offerings of the early-mover public surf parks become the majority of global inventory. The percentage of global inventory running private club models is also likely to grow to significant levels.

Taken together, these developments suggest the surf park industry is no longer being defined by internal debate, but by external demand. Over the next 24 months, growth will be driven less by proving what’s possible and more by responding to real-world forces: capital seeking differentiated experiential assets, developers looking for durable lifestyle anchors, and wave technologies flexible enough to work across very different markets. Not every project will succeed, and not every model will travel—but by the end of 2027, the industry will bear little resemblance to the one that spent a decade asking whether surf parks could work at all. The question now is which formats, partnerships, and technologies will hold up at scale.

You must be logged in to post a comment Login