While the surf park industry promotes fun and active outdoor lifestyles, these developments come with certain risk factors. Experienced developers know the risks extend far beyond the waves. Figuring out what needs insurance can get complicated. That’s where Granite Insurance comes in.

With years of experience in outdoor action sports, Granite Insurance has grown alongside industries like rock climbing and whitewater rafting. So when surf parks began to rise in popularity, stepping into this new wave of development was a natural fit.

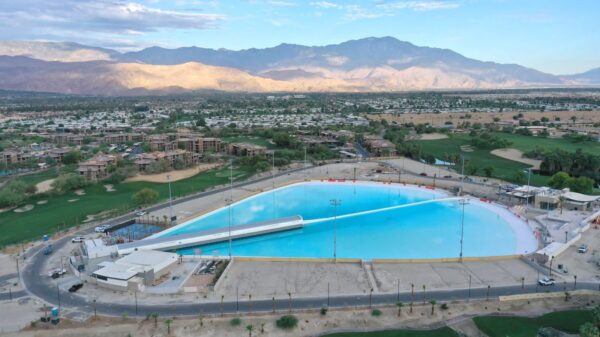

Surf Park Central spoke with Cameron Annas, Granite Insurance’s CEO, to learn more about insuring large investments that protect guests and organizations.

Surf Park Central: To get started, can you tell me about Granite Insurance and what you offer?

Cameron Annas: Granite Insurance is a boutique national insurance firm that specializes in the adventure and entertainment industry. We trace our roots back to 1936, but our adventure sports practice really started about 12 years ago in the zipline industry. Today, we insure roughly 75% of the zipline operations in the U.S., and we’ve expanded into other sectors like whitewater rafting, indoor climbing gyms, water sports, resorts, and campgrounds. Now, we’re excited to bring that experience to the surf park world, which is a newer frontier from an insurance standpoint.

Surf Park Central: Aside from the obvious risks that come with action sports, why do surf parks need specialized insurance? And how do you tailor that coverage to fit their needs?

Annas: The two biggest risks we see are guest injuries at the facility and physical damage to the property from events like wind, fire, or earthquakes. Injuries can lead to liability issues, and property damage can stop revenue, which affects your ability to pay lenders and investors.

Underwriters are still unfamiliar with surf parks, so there’s a lot of education involved. They often assume worst-case scenarios—drownings and concussions are at the top of their list. It’s important for operators to proactively address those concerns with documented plans. If the underwriter asks the question before you’re ready, it’s already a red flag.

One risk that often gets overlooked is pollution. In insurance terms, a pollutant can include bacteria or viruses. So water quality issues, like brain-eating amoeba or legionella, are real concerns. Most standard liability policies don’t cover these, so we make sure surf parks have that carved out with specific coverage.

Surf Park Central: That reminds me of the whitewater park near Charlotte, North Carolina, that had an incident a few years ago. It really changed how those facilities are regulated by local governments.

Annas: Exactly. That came down to filtration and water quality—two things every surf park needs to take seriously.

Surf Park Central: Surf parks today aren’t just about surfing. A lot of them are adding things like paddleboarding, climbing walls, and even restaurants. How do these added amenities impact risk and insurance planning?

Annas: Great question. Anytime you’re adding a new activity, you need to do a cost-benefit analysis. What’s the projected revenue, and what’s the cost to insure that activity?

Take trampolines, for example. They’re notoriously expensive to insure. If a family entertainment center adds even a small trampoline setup, the minimum premium could be $100,000. If it only brings in $10,000 in revenue, that’s not sustainable.

Also, your operating procedures need to be updated for any new activity. Staff need to be trained, and your insurance advisor should be part of that conversation before you invest in new equipment.

In terms of what fits with surf parks, climbing walls, pump tracks, and skateboarding all make sense culturally. But you also have to think about how each of those gets rated in your insurance policy. You don’t want food and beverage revenue to be rated the same as surf operations—that would drive your costs up unnecessarily.

Surf Park Central: From your perspective, what are some of the biggest mistakes you’ve seen surf park developers make so far?

Annas: The biggest one is underbudgeting for insurance. We’ve seen developers get lowball estimates up front from brokers trying to win their business, only for the actual cost to come in three times higher. That’s a tough situation to be in late in the process.

Another issue is going to market without clear standard operating procedures. Underwriters price for uncertainty. If your safety protocols, training programs, and risk management plans aren’t clearly documented, you’ll pay more for coverage.

And lastly, I’d warn against overcommitting on liability coverage because of pressure from lenders or landlords. Too much required coverage can make a business financially unviable, especially in such a new industry.

Surf Park Central: If someone’s just starting out and thinking about building a surf park, what advice would you give them?

Annas: Talk to us early. We spent over a year studying the surf park industry so we could build a program that adjusts premiums based on specific risk factors.

For example, we offer better rates for surf areas that have foam padding over concrete or for surfaces that are slip-resistant. If a developer knows those things before construction starts, they can make smarter design decisions that save them millions in insurance over time.

Surf Park Central: That’s a huge incentive to plan ahead. Have you seen any good examples of what surf parks are doing right so far?

Annas: Definitely. The most successful operators we’ve seen have well-developed lifeguard training programs. Underwriters want to know who’s training the staff, how often, and whether it’s in-house or third-party.

Positioning of instructors and lifeguards is also key, especially in high-impact zones. And access prevention is another big one. How do you keep people out of the water after hours or during unassigned time slots? How do you prevent unauthorized guests from slipping into the pool area? Operators that have clear plans for those issues are ahead of the game.

Surf Park Central: For anyone looking to get in touch with you or Granite Insurance, what should they know?

Annas: We’re an advisor and broker, so we don’t underwrite the insurance ourselves—we design solutions and work with carriers to take on the risk. Right now, there are only about five insurance companies willing to cover surf parks. And the pricing between them can vary by 400%.

We’ve actually brought two new insurance companies into the surf park space by educating them on the risks and operations. That’s a big part of the value we bring—we’re not just moving paper, we’re helping shape the insurance market for this industry.

Learn more about Granite Insurance.

You must be logged in to post a comment Login